The federal government handed down its 2019-20 federal budget last night. We look at some of the key relevant sections of the budget and how that impacts you.

Personal Income Tax plan

The government is seeking to extend the amendments proposed in the 2018-19 Budget as follows;

From 1 July 2018 – 30 June 2022

-

An increase to the Low to Middle Income Tax offset (LMITO) from a maximum of $530 to $1,080. This is in addition to the Low-Income Tax Offsets (LITO) and will be received once a tax return is lodged in that income year.

From 1 July 2022

-

The government is proposing to increase the upper threshold of the 19% tax bracket from $41,000 to $45,000

-

A proposed increase of the Low-Income Tax Offset (LITO) maximum amount from $645 to $700. Do note that this increase will be withdrawn by 5 cents per dollar between taxable incomes of $37,500 and $45,000 and further be withdrawn at a rate of 1.5 cents per dollar between taxable incomes of $45,000 and $66,667.

From 1 July 2024

-

The government is proposed to reduce the 32.5% marginal tax rate to 30%.

-

The 37% tax bracket will also be abolished as already legislated.

So What?

-

If you’re eligible for LMITO, you could qualify for a refund after you submit your tax returns.

-

These tax changes are intended to reduce the income tax rates for many Australians over the stated period. The government estimates that about 94% of Australians paying tax will pay 30% tax or less from 1 July 2024.

-

For people on incomes at $200,000 there could be potential tax savings of $5,672

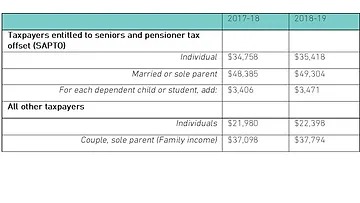

Medicare Levy

-

The government proposes to increase the Medicare levy’s low-income thresholds for 2018-19 income year.

So What?

-

With the increased threshold, you wont be charged the Medicare Levy is you taxable income is below the following;

Superannuation

From 1 July 2020

-

People aged 65 and 66 can make voluntary contributions into super without satisfying the work test

-

People under age 67, at any time during a financial year, can trigger the non-concessional bring forward rule. It is important to note that this continues to be subject to a person’s superannuation balance being under the threshold to be able to trigger the bring forward rule.

-

The government is proposing that a spousal contribution can be made where the receiving spouse is under age 75. Where the receiving spouse is 65, 66 years of age, they do not have to satisfy the work test. However, they’ll have to meet the work test from age 67

-

The government is seeking to amend the Tax Act 1997 to allow trustees of super funds, particularly SMSFs, with assets in both accumulation and pension phases to choose their preferred method of calculating Exempt Current Pension Income (ECPI)

From 1 October 2019

-

The government has introduced a Bill to give effect to elements of Protecting Your Super measures which were removed from the original Bill already legislated. If this were to pass, it will mean that the law will prohibit trustees of superannuation funds from offering insurances on an opt-out bases for;

-

New members under age 25 who open accounts on or after 1 October 2019, and

-

Members with balances less than $6,000.

So What?

-

Allowing contributions will mean that if eligible, you can continue to grow your superannuation benefits for retirement up to age 67.

-

Having the ability to make a spousal contribution for a further 5 years extends the opportunity to equalise superannuation balances between spouses and provides a further extension a spouse may claim a tax offset for the contributions.

-

If these measures are legislated, it’ll help stop small superannuation balances being eroded by insurance premiums.

We’re here to help you make sense of all these changes. If you want to discuss this or any other Financial Advice matters, do reach out to us.

General Advice Disclaimer

Note: – this information is of a general nature only and does not take into account your objectives, financial situation or needs. Please consult a qualified Financial Adviser and a Tax Accountant before making any decisions on the basis of this information. Wealth Peak Financial Advice Ltd ABN: 24 615 007 326, is a Corporate Authorised Representative of Total Financial Solutions Ltd. AFSL 224954 and ABN 94 003 771 579